The global climate finance landscape involves a mix of public and private funding supporting climate mitigation and adaptation efforts. Funds are channeled through bilateral agencies, multilateral banks, climate funds, and private investors. Public finance mainly consists of grants and concessional loans for vulnerable countries, while private finance focuses on commercial investments. However, most funding still favors mitigation over adaptation. Despite some progress, overall climate finance falls short of global needs, underscoring the need to scale up, improve access, and ensure fairer distribution, especially for developing nations.

Global Climate Funding Flows

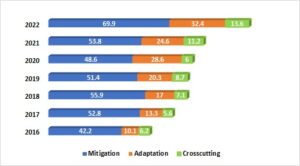

The Climate Policy Initiative (CPI) estimates that between USD 6.7 – 10 trillion in annual climate finance will be needed through 2050 to effectively mitigate and adapt to climate change. This funding is essential to limit global warming to below 1.5°C and prevent the most severe impacts of climate change. Currently, the majority of climate finance is allocated towards mitigation efforts, particularly renewable energy with a smaller share directed to adaptation, which remains crucial for vulnerable countries.

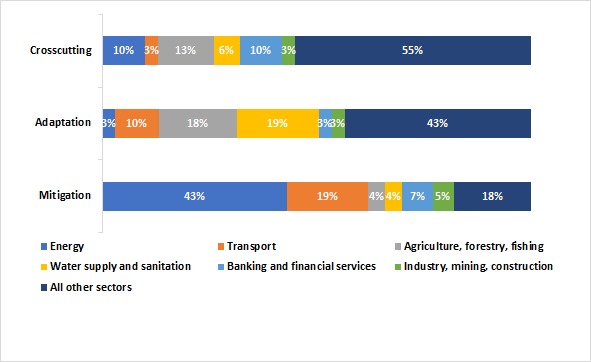

Since 2016, sectoral distribution trends have remained largely consistent. Most mitigation finance has been concentrated in the energy and transport sectors. From 2016 to 2022, these two sectors accounted for over 62% of the total mitigation finance provided and mobilized. In contrast, adaptation finance has been more evenly spread across a wider range of sectors. Notably, the water supply and sanitation sector, together with agriculture, forestry, and fishing, represent the largest shares 19% and 18% respectively of total adaptation finance provided and mobilized.

Figure 1. Climate finance provided and mobilized between 2016-2022 as per climate theme (USD billion)

Source: OECD, 2024

Source: OECD, 2024

Figure 2. Sectoral distribution of climate finance provided and mobilized between 2016-2022

Source: OECD, 2024

Source: OECD, 2024

Channels of International Climate Financing

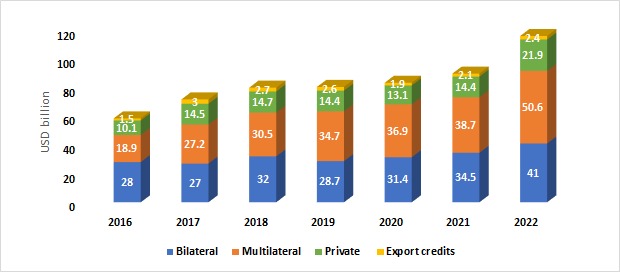

From 2016 to 2022, bilateral climate finance increased from USD 28 billion to USD 41 billion, showing steady growth after 2020 despite some fluctuations. Multilateral finance more than doubled during this period, reaching USD 50.6 billion in 2022, mainly due to contributions from multilateral development banks. Private finance remained around USD 14 billion until 2021, then rose sharply to USD 21.9 billion in 2022, a 52% increase, reflecting renewed private sector engagement. Climate-related export credits remained small and unstable, totaling USD 2.4 billion in 2022.

Figure 3. Channels wise climate finance provided and mobilized between 2016-2022 (USD billion)

Source: OECD, 2024

Source: OECD, 2024

Instruments of International Climate Financing

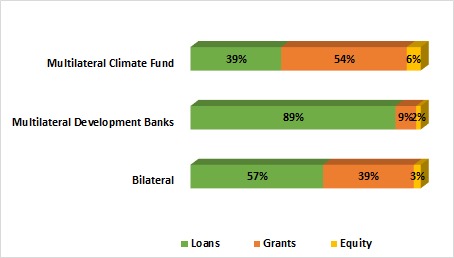

Different types of providers employ various funding instruments aligned with their distinct roles, resulting in diverse activities within their portfolios. Between 2016 and 2022, nearly 90% of financing from Multilateral Development Banks (MDBs) was disbursed as loans. In contrast, multilateral climate funds and bilateral providers maintained a more balanced allocation between loans and grants. Specifically, multilateral climate funds allocated approximately 39% of their funding as loans and 54% as grants, while bilateral providers allocated 57% as loans and 39% as grants. These two categories of providers typically support a broader and more diverse range of projects and activities.

Figure 4: Public Climate Finance provided between 2016-2022 as per financial instruments (USD billion)

Source: OECD, 2024

Source: OECD, 2024